Buying a Home in Texas: Credit Score Requirements & Loan Options

What Credit Score Do You Need to Buy a Home in Texas?

Understanding credit requirements is one of the most important, and often misunderstood, parts of buying a home in Texas. While buyers frequently assume they need “perfect” credit to qualify, the reality is more nuanced. Credit scores influence not only loan eligibility, but also interest rates, monthly payments, mortgage insurance costs, and long-term affordability.

This guide breaks down credit score requirements by loan type, explains how lenders evaluate risk in Texas, and outlines how buyers can position themselves strategically before entering the market.

How Lenders Use Credit Scores

A credit score is a numerical representation of how a borrower has managed debt over time. Mortgage lenders use it to assess repayment risk alongside income, assets, employment history, and debt-to-income ratio.

In practice, credit scores affect three key areas:

1. Approval thresholds set by loan programs and individual lenders

2. Interest rates and pricing adjustments

3. Mortgage insurance requirements and costs

Even small differences in score can materially change borrowing costs over the life of a loan.

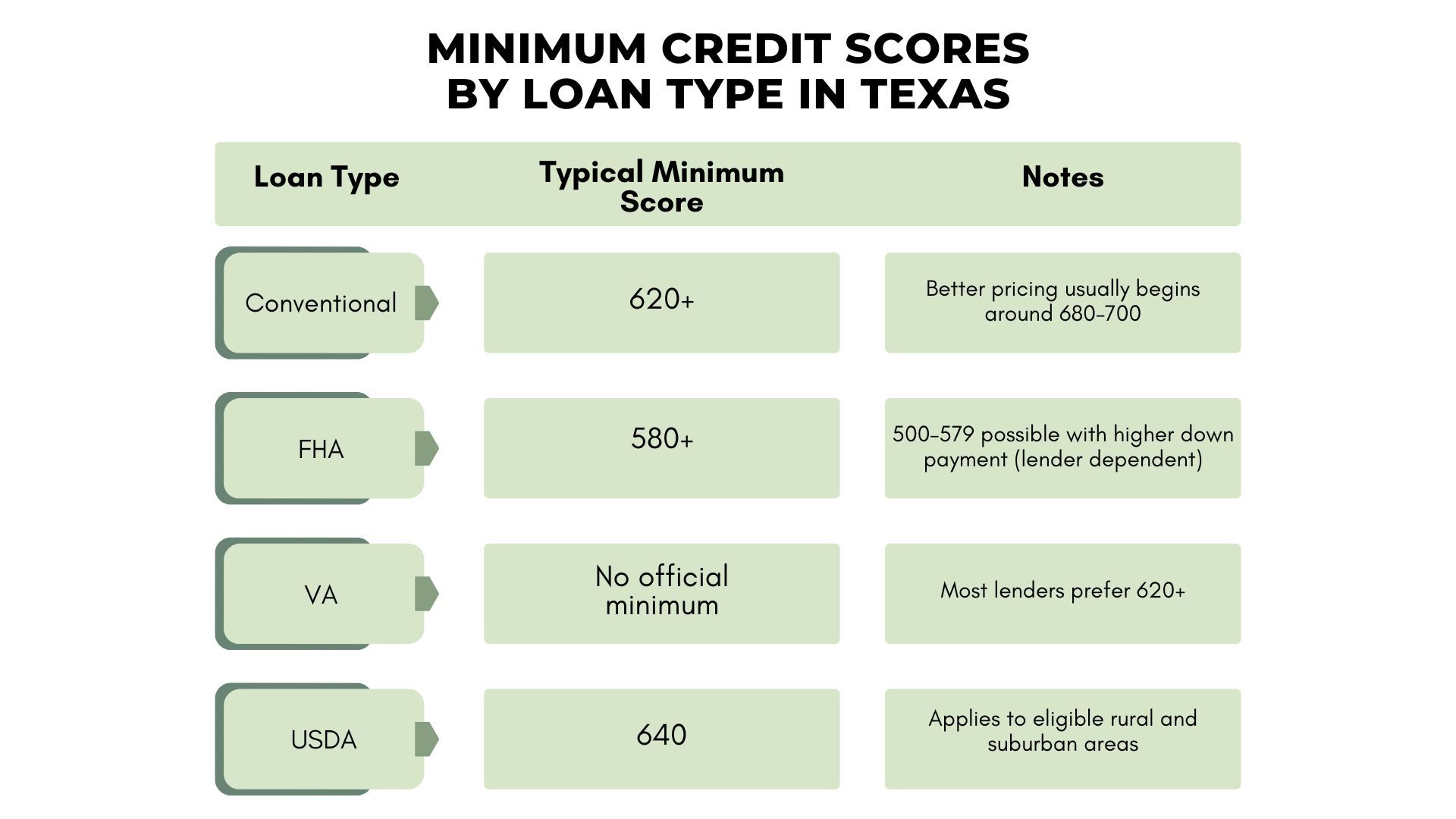

Credit Score Requirements by Loan Program

Different loan programs serve different buyer profiles, and each comes with its own credit expectations. The table below reflects commonly used minimums in Texas. Individual lenders may impose higher standards based on risk tolerance and market conditions.

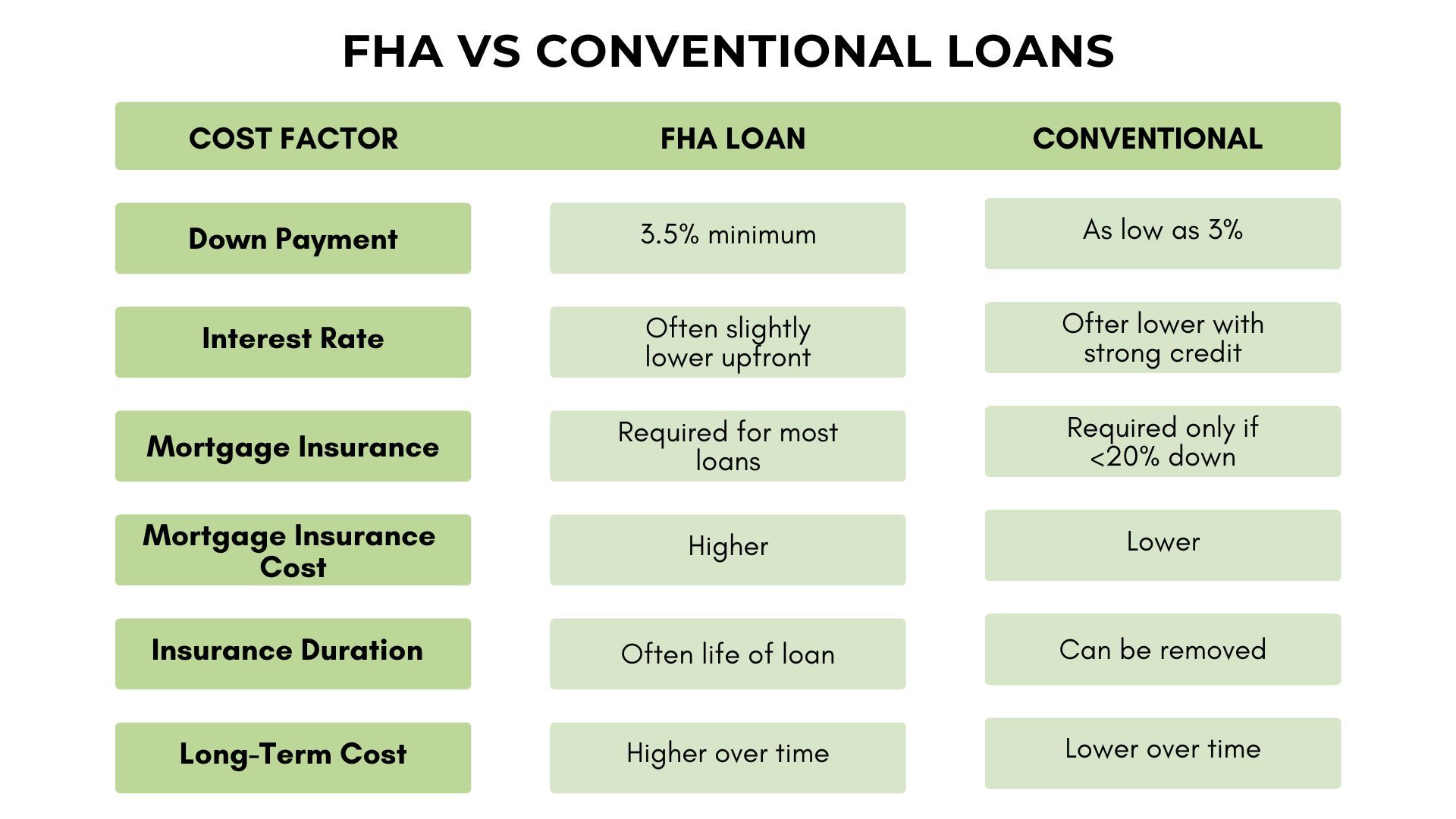

Conventional Loans: Where Credit Has the Biggest Impact

Conventional financing is the most sensitive to credit score differences. While 620 is often cited as the minimum threshold, borrowers with scores below 680 typically face higher interest rates and private mortgage insurance premiums.

For example, industry data consistently shows that borrowers with credit scores in the low 700s may secure interest rates that are 0.50%–0.75% lower than borrowers near the minimum qualifying score. On a typical Texas home price, that difference can translate into tens of thousands of dollars over a 30-year loan.

This is why many buyers benefit from delaying their purchase briefly to improve credit before locking in financing.

FHA Loans: More Flexible, Higher Ongoing Costs

FHA loans are widely used by first-time buyers in Texas because of their lower credit barriers and modest down payment requirements. However, FHA mortgage insurance premiums apply both upfront and annually, regardless of credit score.

While FHA allows access to homeownership with mid-range credit, it is often best viewed as a stepping-stone loan, with the goal of refinancing into conventional financing once credit improves and equity is built.

VA and USDA Loans: Specialized but Powerful Options

VA loans offer one of the strongest financing tools available, especially for eligible veterans and active-duty service members. While the VA does not set a minimum credit score, most Texas lenders apply internal standards. Strong credit improves rate options, but even moderate scores may qualify with competitive terms.

USDA loans, designed for rural and semi-rural areas, require slightly higher credit standards but offer zero-down financing. Many buyers are surprised to learn that parts of the outer Houston metro still qualify.

To see USDA eligibility, input your address here.

Credit Score vs. Debt-to-Income in Texas

Texas buyers face higher-than-average property taxes, which means lenders place significant emphasis on debt-to-income (DTI) ratios. A strong credit score alone does not guarantee approval if monthly obligations are too high.

In many cases, buyers with moderate credit but low debt outperform higher-credit buyers with heavier monthly liabilities. This reinforces the importance of evaluating the full financial picture, not just the score.

Improving Credit Before Buying

Credit improvement does not require years in most cases. Many buyers see meaningful score gains within one to three months by focusing on utilization ratios, correcting reporting errors, and avoiding new credit inquiries.

-

Days 1–30: Stabilize

- Bring accounts current and stop late payments

- Dispute errors and set autopay -

Days 31–60: Improve

- Pay down credit cards below 30% utilization

- Avoid new credit inquiries -

Days 61–90: Optimize

- Maintain low balances and steady payments

- Prepare for lender review or pre-approval -

What to Expect

- Potential improvement of 20–60+ points

- Better loan options and buying power

With the right plan and timing, credit improvement is often a manageable, strategic step that helps buyers move forward with confidence rather than delay their home purchase.

Why This Matters in the Texas Market

Texas remains a high-growth state with competitive housing pockets, particularly in Greater Houston. Credit strength directly affects a buyer’s ability to compete, negotiate, and absorb costs such as taxes and insurance.

Buyers who understand their credit position early are better equipped to:

- Structure offers confidently

- Compare loan scenarios accurately

- Avoid payment shock after closing

- Plan refinances and long-term equity strategies

Credit Score Recap

There is no single “right” credit score to buy a home in Texas. The best path depends on loan type, financial structure, timing, and long-term goals. What matters most is clarity, knowing where you stand and what options align with your situation.

At Newcomb Realty Group, we help buyers evaluate credit readiness, coordinate with reputable Texas lenders, and build purchase strategies rooted in data, not pressure. Whether you are ready now or planning ahead, informed decisions create stronger outcomes.

If you are considering buying in Texas and want a clear, realistic assessment of your options, our team is here to guide you every step of the way.

📞 Book a consultation call: 832-779-5478

🌐 Visit our website: www.newcombrealtygroup.com

📲 Connect with us: Instagram | Facebook | TikTok | YouTube | LinkedIn

Categories

Recent Posts

Realtor® Listing Specialist and Team Lead | License ID: 634969

+1(832) 779-5478 | kristina.newcomb@exprealty.com