What First-Time Buyers Wish They Knew Before Buying a Home

What First-Time Buyers Wish They Knew Before Purchasing a Home

Buying your first home is exciting, but it can also feel overwhelming when you do not know where to start or how the process really works. Most first-time buyers are not unprepared. They are simply unfamiliar with the decisions, costs, and timing involved.

After working with first-time buyers across the Houston area and nearby suburbs, the same thoughts come up again and again after closing. Not regrets, but things they wish had been explained earlier.

This guide is written for someone starting from the very beginning, with no assumptions and no pressure.

Where Do You Actually Start?

Most first-time buyers start by scrolling listings online. While browsing homes can be fun, it is not the best place to begin. The real first step is understanding what monthly payment feels comfortable for your life, not just what a lender says you can qualify for.

In Texas, property taxes and insurance vary by area and can materially change your monthly payment. Setting a realistic monthly budget before shopping helps you narrow your search and avoid stretching too far. It also makes your conversations with lenders and agents more productive.

To better understand what goes into monthly ownership costs, check out our detailed guide on what the real cost of homeownership looks like in Texas.

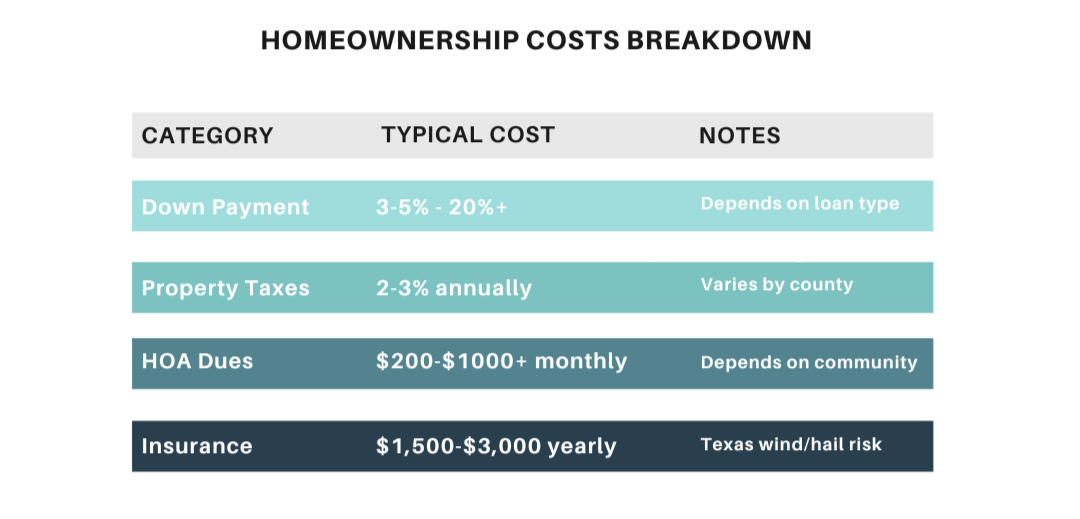

How Much Money Do You Really Need to Buy?

A common myth is that you have to save 20 percent down to buy a home. While putting 20 percent down may reduce monthly mortgage insurance and give you competitive loan pricing, many first-time buyers purchase with much less depending on their loan program. FHA, conventional, and other low-down payment options exist.

What often surprises buyers is cash-to-close, which includes:

-

Down payment

-

Closing costs (typically 2 percent to 6 percent of the purchase price in Texas)

-

Prepaid taxes and insurance

-

Inspection and appraisal fees

For example, on a $300,000 home, closing costs alone could range above $6,000 to $18,000, depending on the loan and services included. Understanding these numbers early makes the process feel manageable instead of stressful.

There are also Texas-specific assistance programs that help first-time buyers with down payment or closing costs, such as statewide grants or local city programs. Checking eligibility can make homeownership more accessible.

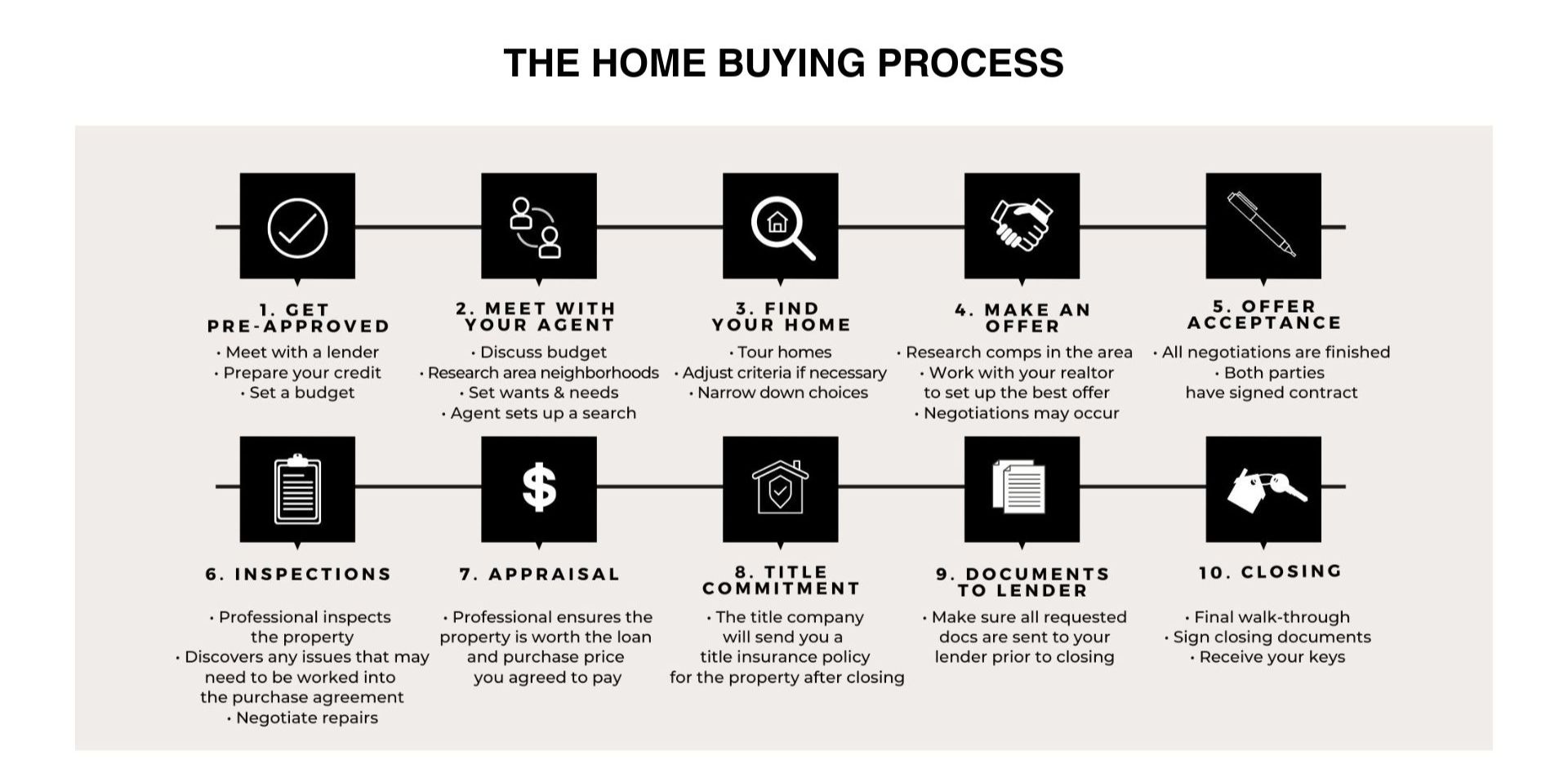

Pre-Approval vs Pre-Qualification

Before you start touring homes, get pre-qualified or pre-approved by a lender. These terms are often used interchangeably, but they are not the same:

-

Pre-qualification gives a rough estimate of how much a lender might lend based on information you provide.

-

Pre-approval involves documentation, income and credit review, and results in a stronger letter that tells sellers you are serious.

A strong pre-approval makes your offer more competitive and helps you avoid surprises later in the process.

Monthly Payments Are Not the Only Costs

Your mortgage payment is only one part of what it costs to own a home. Over time, homeowners also experience changes in property taxes, adjustments to homeowners insurance, routine maintenance expenses, and utilities. In some neighborhoods, HOA fees are also part of the monthly picture.

Even newer homes require upkeep, and costs can evolve as the home ages.

Many first-time buyers later wish they had planned beyond the first year and thought about what ownership looks like three to five years down the road. Preparing for ongoing expenses early helps avoid financial surprises and makes ownership feel more manageable.

Don’t Underestimate Maintenance

Renting and owning feel very different once you move in. When you rent, repairs are handled by a landlord. When you own, that responsibility becomes yours.

Routine maintenance is not always expensive, but it is consistent. Items like HVAC servicing, filter replacements, plumbing and electrical upkeep, roof wear, and exterior maintenance all add up over time. Landscaping, gutter cleaning, and exterior paint are easy to overlook but part of long-term ownership.

Many experienced homeowners recommend setting aside roughly one percent of the home’s value each year for maintenance and repairs. Having a small reserve creates confidence and allows you to address issues early rather than waiting until they become costly problems.

For a seasonal home maintenance guide, see here.

Home Inspections Are Not Optional

Waiving a home inspection to make an offer more attractive may seem tempting, but it often leads to regret later. A professional inspection provides information you cannot see during a showing and helps buyers understand the true condition of the home.

Inspections can uncover issues related to the roof, foundation, HVAC systems, electrical components, plumbing, and potential pest concerns. In Texas, inspection costs typically range from a few hundred dollars depending on the size and complexity of the home.

Beyond identifying problems, inspections help buyers plan for future maintenance and create leverage during negotiations. Smart buyers use inspection findings to ask informed questions, request repairs or credits, and move forward with confidence.

Evaluating Long-Term Fit

It is easy to fall in love with finishes, paint colors, or upgraded kitchens. What tends to matter more over time are the factors that influence comfort and resale.

Location plays a significant role in long-term value, as do neighborhood stability and access to schools, even for buyers without children. Layout and functionality matter as life changes, and commuting patterns or future development can affect how a home fits into daily routines.

Your first home does not need to check every box. It should support your life today and still make sense when you are ready for your next chapter.

The Contract and Timeline

Real estate contracts include deadlines, contingencies, and legal obligations that many first-time buyers are unfamiliar with. Important elements include:

-

Earnest money — a deposit showing serious intent

-

Option period — your window to inspect and back out

-

Contingencies for appraisal, financing, and inspection

-

Closing disclosure and paperwork review

Missing deadlines or misunderstanding contract terms can cost money or jeopardize your offer. Knowing the timeline, from accepted offer to closing (often around 30 to 45 days), helps manage expectations.

Market Timing Isn’t Perfect

Many first-time buyers worry they will buy at the “wrong time.” The truth is there is no perfect market. Real estate is a long-term investment, and waiting for ideal conditions often leads to higher prices or missed opportunities.

Smart buyers focus on homes that fit their needs and budgets, rather than timing the market.

What First-Time Buyers Wish They Knew Most

When first-time buyers reflect after closing, the biggest takeaway tends to be clarity.

They wish they had:

1. Asked more questions early

2. Focused on realistic monthly costs

3. Understood the full scope of expenses

4. Worked with professionals who explained the “why,” not just the “what”

You don’t have to know everything to buy your first home. You need informed guidance and thoughtful planning.

First-time buyers make up a large part of the clients we serve. From understanding true monthly costs to navigating inspections, contracts, and closing, we guide buyers through the process daily and know how to anticipate challenges before they become stress points.

If you want experienced guidance and clear answers from the start, we’d love to walk you through what buying your first home could look like.

Connect with us!

📞 Book a consultation call: 832-779-5478

🌐 Visit our website: www.newcombrealtygroup.com

📲 Connect with us: Instagram | Facebook | TikTok | YouTube | LinkedIn

Categories

- All Blogs (82)

- Conroe (2)

- Cypress (13)

- Dallas-Fort Worth (2)

- Hockley (5)

- Home Ownership Information (30)

- Houston (9)

- Katy/Fulshear (10)

- Magnolia (4)

- Market Forecast (12)

- Memorial (2)

- Neighborhood Information (40)

- New Caney (2)

- Pearland (3)

- Relocation Guide (39)

- Retiree Relocation (3)

- Richmond (3)

- Spring (5)

- Sugarland (2)

- The Woodlands (6)

- Tomball (6)

- Waller (2)

Recent Posts

Realtor® Listing Specialist and Team Lead | License ID: 634969

+1(832) 779-5478 | kristina.newcomb@exprealty.com